No, Government Debt isn't a Crisis

Good Policies that Increase the Deficit are Fine

Recently, there has been talk over a possible deal to restore the old R&D Tax Credit in exchange for expanding the Child Tax Credit. Some people have been cautious in their praise of it or even outright doubtful citing our high current debt. These people are wrong.

Into the Weeds on Debt

You’ve probably seen something like the following graph before:

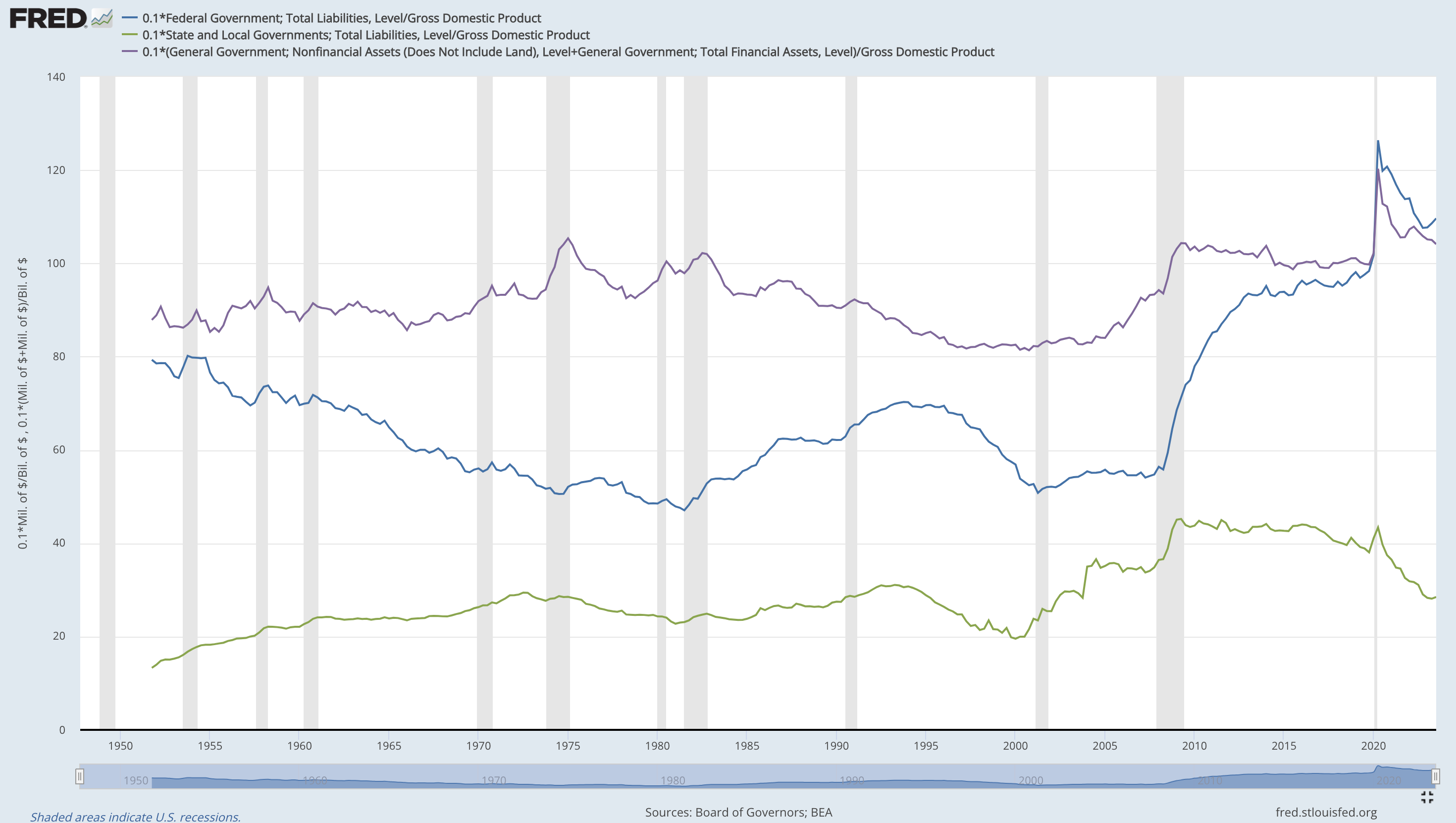

Look at how bad current debt is, scary stuff! One thing I don’t often see is this graph:

Blue is total liabilities of the federal government divided by gross domestic product. See the massive increase at the start of covid that has been working its way down?

Green is total liabilities of state and local governments divided by gross domestic product. During the great recession, they increased and then plateaued while federal debt increased. During covid, they at first increased but then rapidly fell due to the large transfers from federal to state and local governments.

Finally the purple line is total non land assets of all levels of government divided by gdp. It increased in along with everything else in covid and weighs against the increase in debt.

If the federal government creates debt to give money to state and local government, as it did to a great extent during covid, no net government outflows have occurred, it’s just an accounting trick. It doesn’t matter whether money is in a bank account labeled “United States Treasury” or a million labeled something like “Los Angeles Unified School District” if it’s the same amount of money.

So let’s add everything together, all liabilities of federal, state and local government minus all assets(excluding land) of those same levels. If we do that, we get this graph:

What are some things we notice here? From Q1 1981 to Q1 1993, US governments went from owning 27% of the US economy in net assets(excluding land!) to owing 12% in net liabilities for a 39 percentage points total increase(3.25% arithmetic growth per year). Reagan-HW’s profligacy is underrated even by the anti-Reagan types. They were within spitting distance of Q4 1947 by the end, off by 0.5%.

Clinton looks to have presided over a larger decrease than general thought at 20% rather than 10% of gdp(2.5% decrease in net liabilities per year).

Bush Junior is about as bad as assumed at 16% total(2% per year), but the Global Financial Crisis was understandably a large part.

Obama sees a 29% increase during his tenure(3.6% annual). Fiscal Stimulus during the GFC was massive. Although deficit hawks were counterproductive, it was wrong for the fed to put so much of the onus on congress. It’s a shame there were no equity purchases.

The biggest surprise is the relative lack of change during the trump administration pre covid. The federal government ran large deficits but from Q1 2017 to Q1 2020, net liabilities only increased 1.3%(0.4% annually). Including 2020, there is a total increase of 8%(2% annualized) under the trump administration.

The Biden administration so far has seen a 13% drop over 10 quarters for a 5.2% annual drop! Despite large federal deficits, Biden’s robust growth and full employment has not led to a worsening governmental net debt situation. You might claim that this was all due to unexpected inflation devaluing federal debt but price level has increased by 17% over Biden’s term with the federal 2% target wanting to have had only 5% for surprise inflation of 12%. If you take out non financial assets(whose values increase with inflation), you would expect a 14.5 percentage point reversion to 0 if this was an unexpected instant and permanent shock compared to the 13.5 we actually had.

No matter how you slice it, the 2020s recovery was not built off the back of continuous large fiscal outflows and net government debt. Whether you go by total all non land assets and liabilities or just financial assets, Q3 2023 has less net debt than Q4 2019. Both real and nominal interest rates are historically moderate at 1.7% and 4% respectively over a 10 year period.

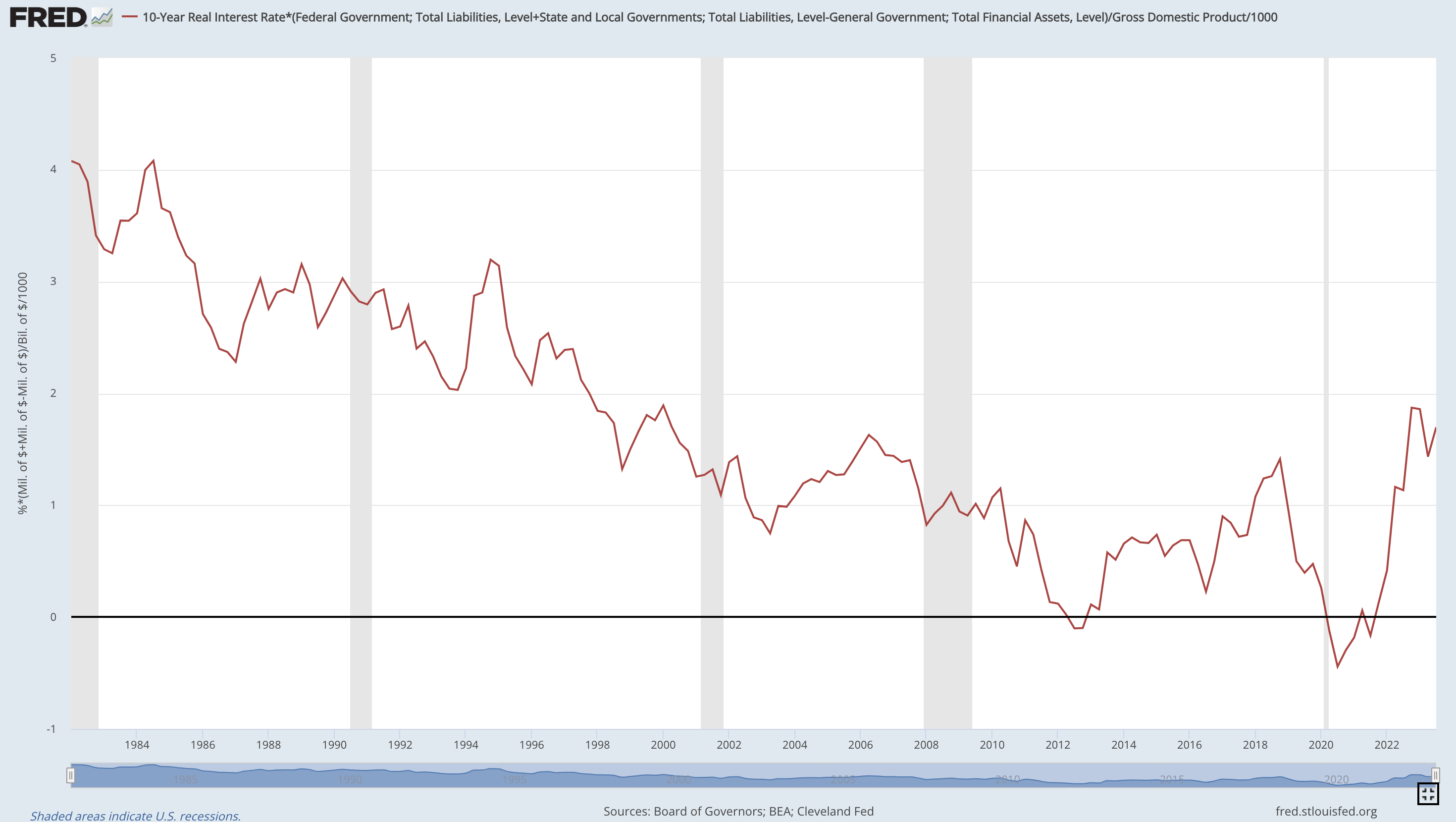

Stable government net debt under W Bush administration level marginal borrowing costs does not a crisis make. Although the level of government debt is unprecedented(in the US), the marginal cost and benefit of reducing said debt is not. To ballpark total borrowing cost, multiply real interest rates by net financial liabilities. If you do that, you get the following graph:

Still not unprecedented. Perhaps ten year real interest rates are hiding that there will be high interest rates after that as boomers retire? Unlikely. 30 year real interest rates imply 2% real interest rates over a 20 year period starting 10 years from now.

Final Thoughts

However, cutting debt can still be a good idea. Continuous reductions in net financial liabilities as a percentage of gdp should push interest rates down further as the Fed is the last mover(a story for another time). Lower interest rates can help push capital deepening, investments in innovation and decarbonization efforts. Tweaks to social security such as eliminating the payroll tax cap or adding a third bend point and decreasing marginal benefits to those receiving more than the poverty line might therefor be worth it. On the other hand, changing the amortization rules of R&D spending has a much larger impact than the corresponding increase in interest rates.

If the tax changes in the works delay fed interest cuts by a month or two, so be it. Incentivizing investments in Total Factor Productivity(R&D Tax Credits) and Labor Supply(Child Tax Credits) is worth the cost.